Quick Answer

Auto financing in Canada lets you buy a vehicle by borrowing from a lender and repaying it over time, usually 36 to 84 months. Lenders review your income, employment, credit history, existing debt, and the vehicle itself — not just your credit score — so many situations, including bad credit, can still qualify.

Buying a vehicle is one of the largest financial decisions many Canadians make. Whether you're buying your first car, replacing your current vehicle, rebuilding your credit, or simply trying to understand how financing works, this guide will help you make a more informed decision.

Auto financing can feel confusing, but the basic idea is simple: you borrow money to purchase a vehicle and repay that amount over time through scheduled payments.

This guide explains how auto financing works in Canada, what lenders commonly consider, how credit scores fit into the process, and what buyers should understand before applying.

What You'll Learn

- What Is Auto Financing?

- How Auto Financing Works

- How Lenders Evaluate Applications

- Understanding Credit Scores

- Understanding Down Payments

- Understanding Interest Rates

- Choosing the Right Loan Term

- Bank vs Dealership Financing

- Special Financing Situations

- Common Mistakes to Avoid

- Frequently Asked Questions

- Your Next Steps

What Is Auto Financing?

Auto financing allows you to purchase a vehicle by borrowing money from a lender and repaying it over time. Instead of paying the full purchase price upfront, you agree to repay the lender according to the terms in your financing agreement.

A typical vehicle financing agreement includes:

| Component | Meaning |

|---|---|

| Vehicle Price | The agreed purchase price |

| Down Payment | Money paid upfront |

| Amount Financed | The balance borrowed |

| Interest | Cost of borrowing |

| Loan Term | Length of repayment |

| Monthly Payment | Scheduled payment amount |

Key Takeaway

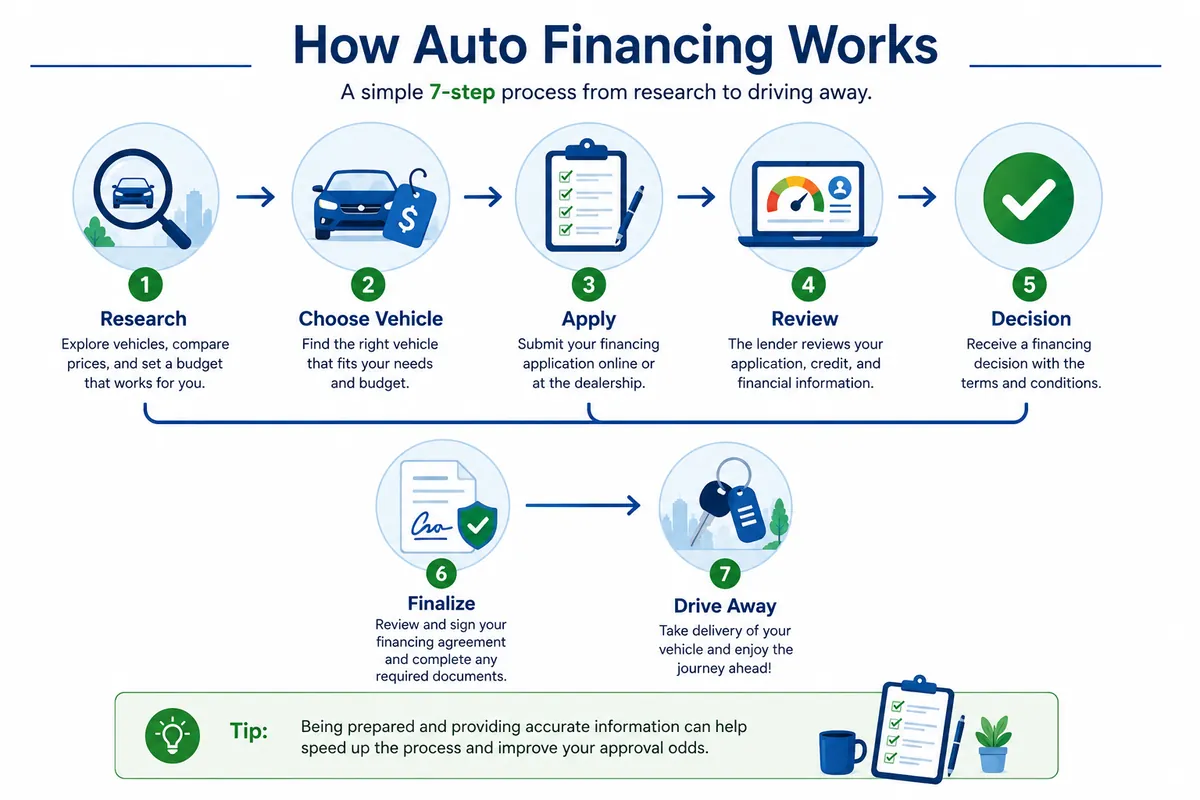

How Auto Financing Works

The vehicle financing process usually follows these steps:

- 1Research vehicles

- 2Choose a dealership or vehicle

- 3Submit an application

- 4Application review

- 5Income or identity verification if required

- 6Financing decision

- 7Review financing terms

- 8Complete documents

- 9Take delivery of the vehicle

The process varies by lender and dealership, but the general journey is similar.

Helpful Tip

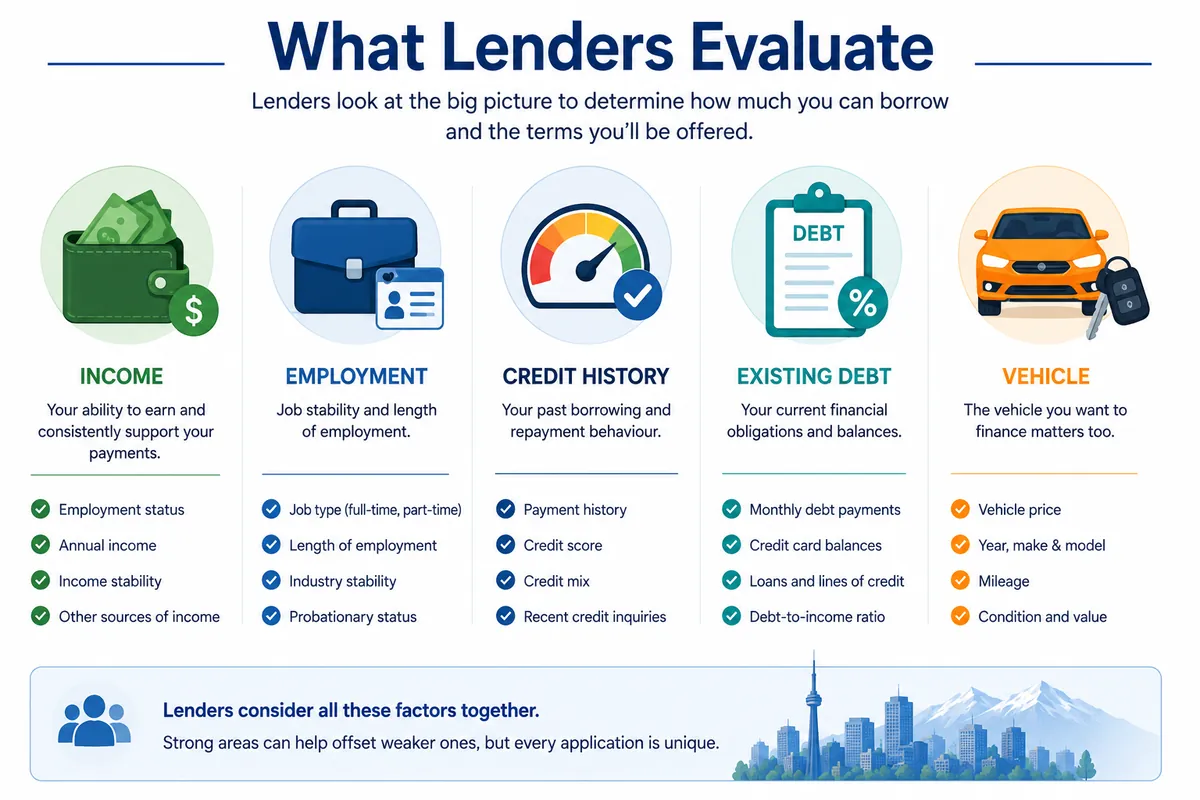

How Lenders Evaluate Applications

Every lender has its own policies. Most lenders review the overall financial picture, not just one factor. Common areas reviewed include:

| Area | What It Means |

|---|---|

| Income | Ability to support payments |

| Employment | Stability and source of income |

| Credit History | Past borrowing behaviour |

| Existing Debt | Current financial obligations |

| Residence | Stability and housing situation |

| Vehicle | Price, age, and loan details |

Did You Know

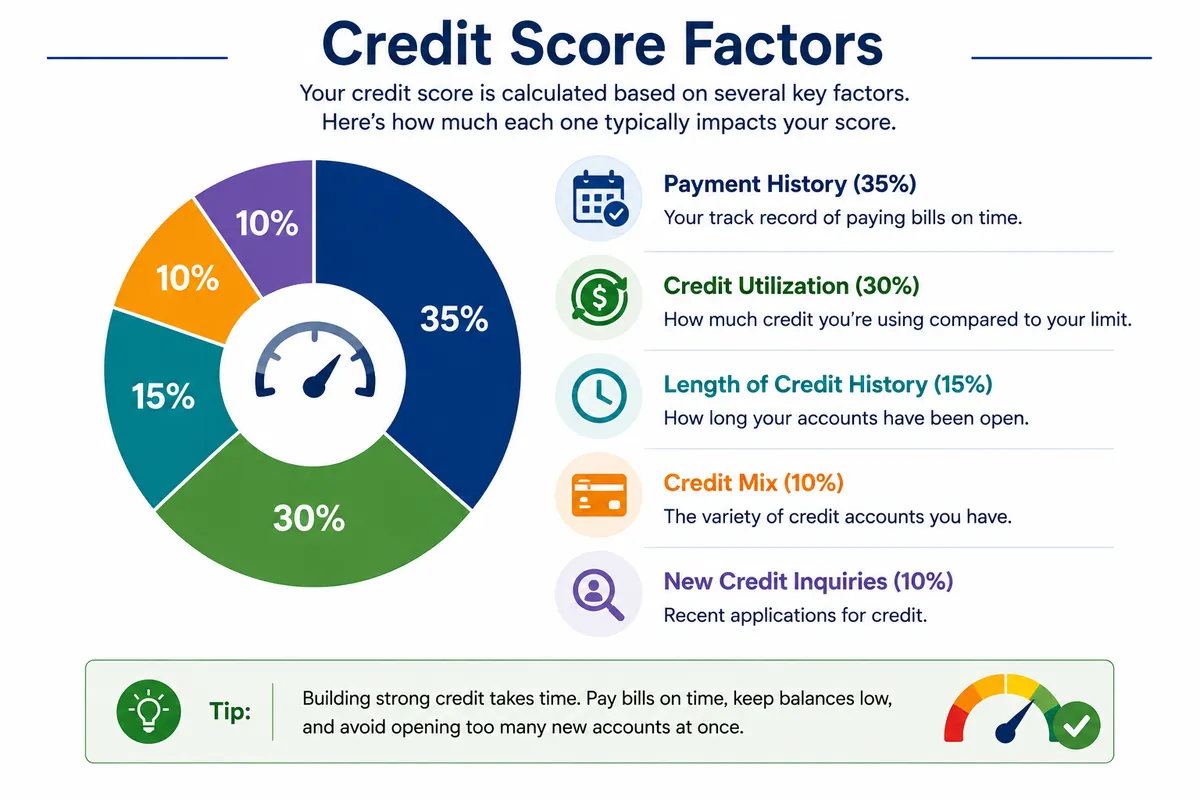

Understanding Credit Scores

A credit score summarizes information in your credit history. Credit history may include:

- Credit cards

- Vehicle loans

- Personal loans

- Mortgages

- Payment history

- Credit utilization

- Recent credit activity

Your credit score is important, but it is not the full story. Lenders may also review income, employment, debts, vehicle details, and affordability.

Common Credit Myths

| Myth | Reality |

|---|---|

| You need perfect credit | Many lenders consider a range of profiles |

| One late payment ruins everything | Lenders review the full application |

| Every lender has the same minimum score | Lender policies vary |

Helpful Tip

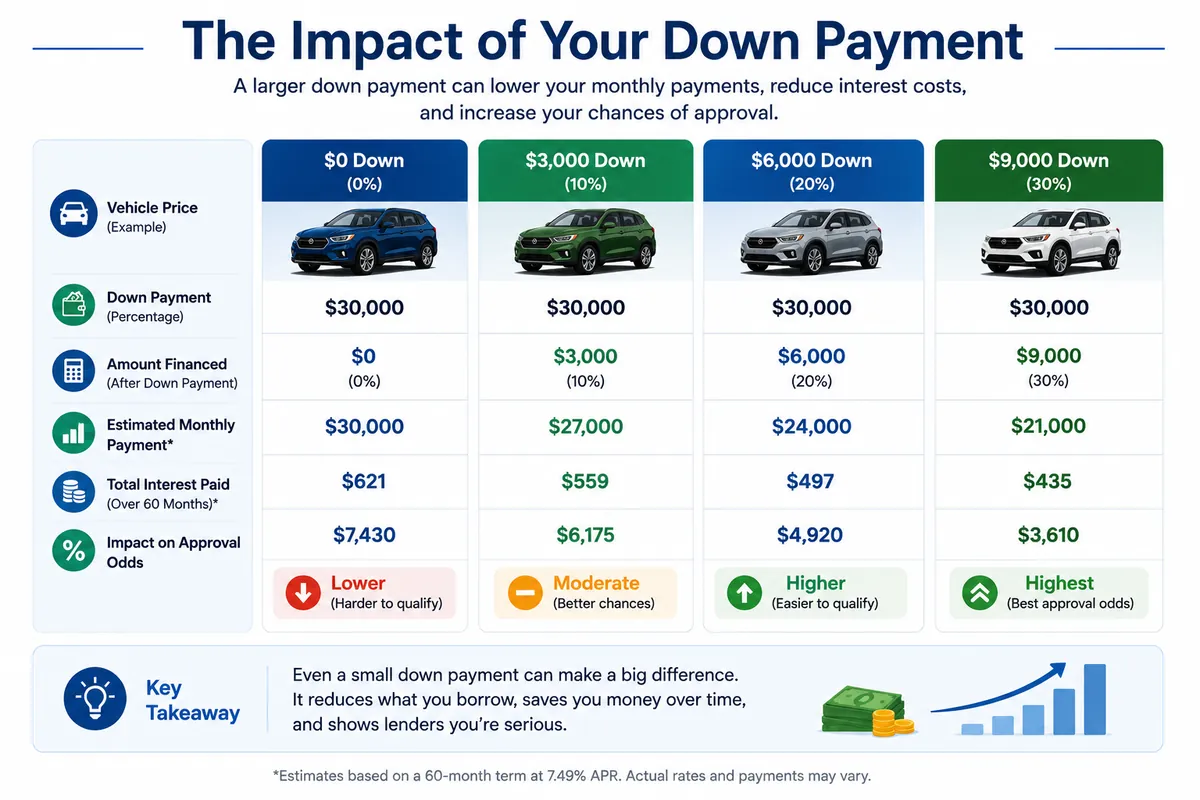

Understanding Down Payments

A down payment is money paid upfront toward the vehicle purchase. A down payment may:

- Reduce the amount financed

- Reduce monthly payments

- Reduce total borrowing cost

- Improve financial flexibility

Common Mistake

Some financing programs may allow no down payment depending on the lender, vehicle, and applicant profile. Learn more in our guide to No Down Payment Car Financing.

Understanding Interest Rates

Interest is the cost of borrowing money. Your financing agreement generally includes repayment of the amount borrowed, interest charges, and any applicable fees or terms.

Factors that may influence financing terms include:

- Credit profile

- Income

- Loan amount

- Vehicle

- Loan term

- Lender policies

- Market conditions

Key Takeaway

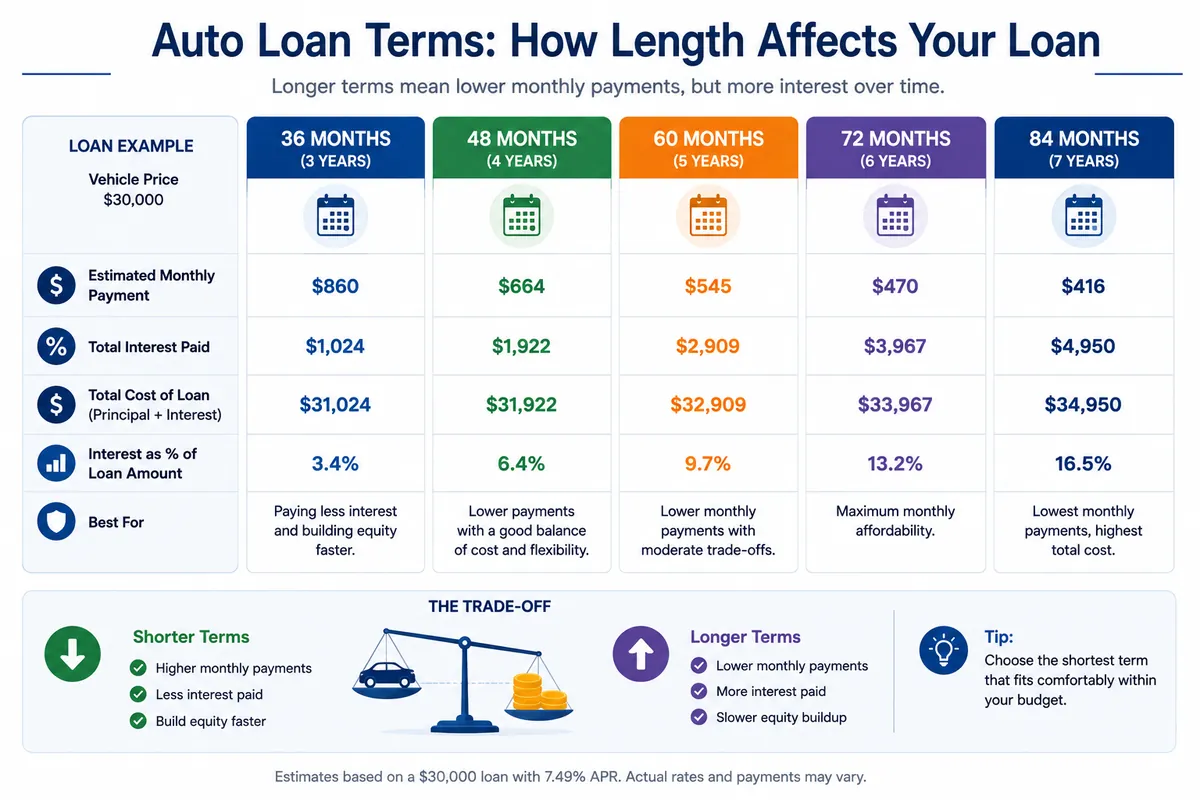

Choosing the Right Loan Term

The loan term is the length of time used to repay the loan. Common terms include:

| Term | Monthly Payment | Total Borrowing Cost |

|---|---|---|

| 36 months | Higher | Generally lower |

| 48 months | Moderate | Moderate |

| 60 months | Moderate/lower | Moderate |

| 72–84 months | Lower | May be higher |

A longer term can reduce monthly payments but may increase the total borrowing cost. The right term depends on budget, financial goals, and comfort level.

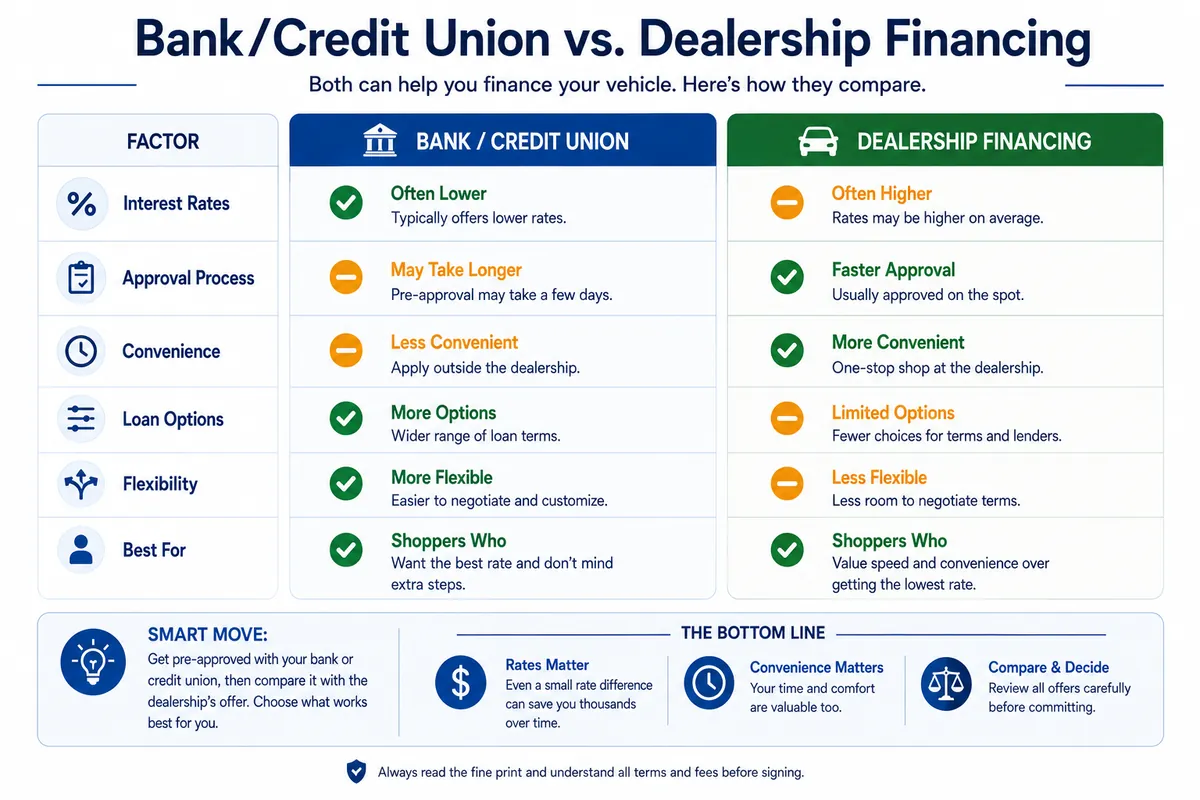

Bank Financing vs Dealership Financing

Canadians often compare bank financing and dealership financing.

| Bank Financing | Dealership Financing |

|---|---|

| Work directly with financial institution | Financing arranged through dealership |

| May be explored before shopping | Vehicle and financing handled together |

| Uses that lender's programs | May access multiple lending partners |

| Buyer manages process directly | Dealership may assist with process |

Key Takeaway

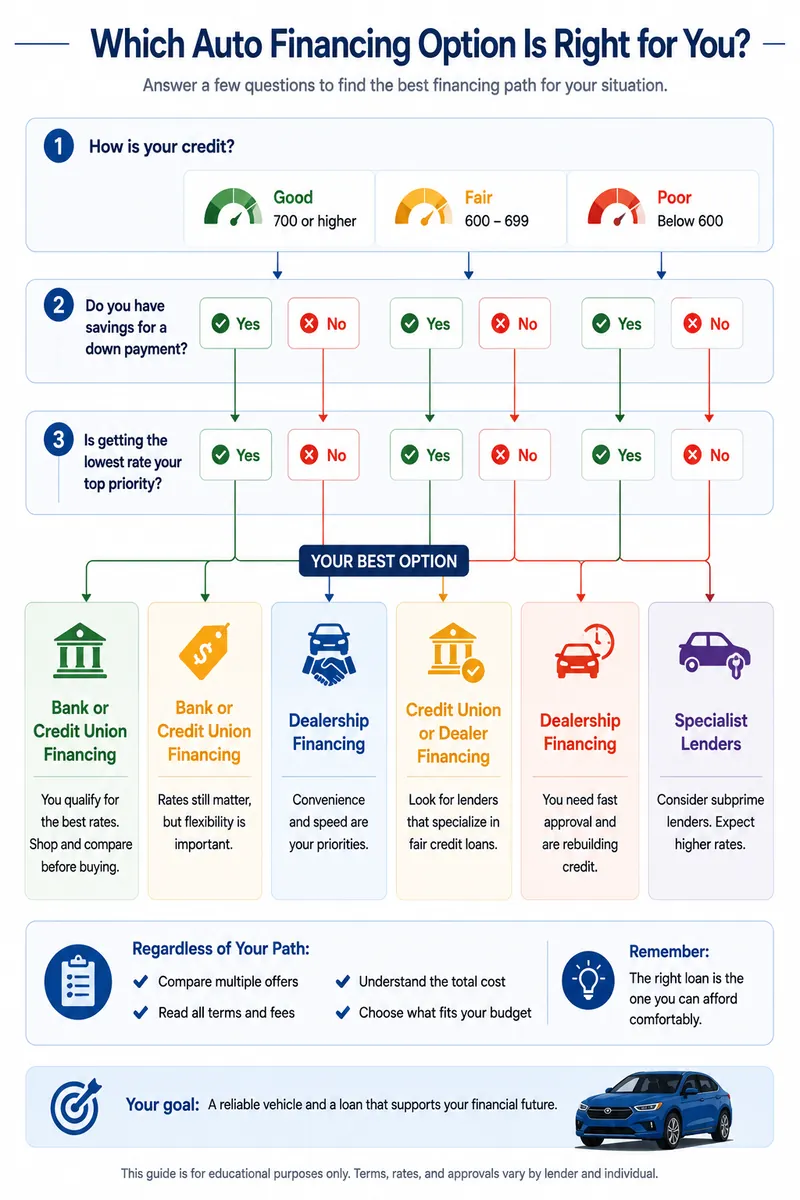

Special Financing Situations

Not every buyer has the same financial background. AutoVoice has dedicated guides for common situations:

| Situation | Guide |

|---|---|

| Rebuilding credit | Bad Credit Car Financing |

| Bankruptcy | Bankruptcy Auto Financing |

| Consumer proposal | Consumer Proposal Car Financing |

| First vehicle | First-Time Buyer Financing |

| Self-employed | Self-Employed Auto Financing |

| New to Canada | Newcomer Car Financing |

| No down payment | No Down Payment Car Financing |

Did You Know

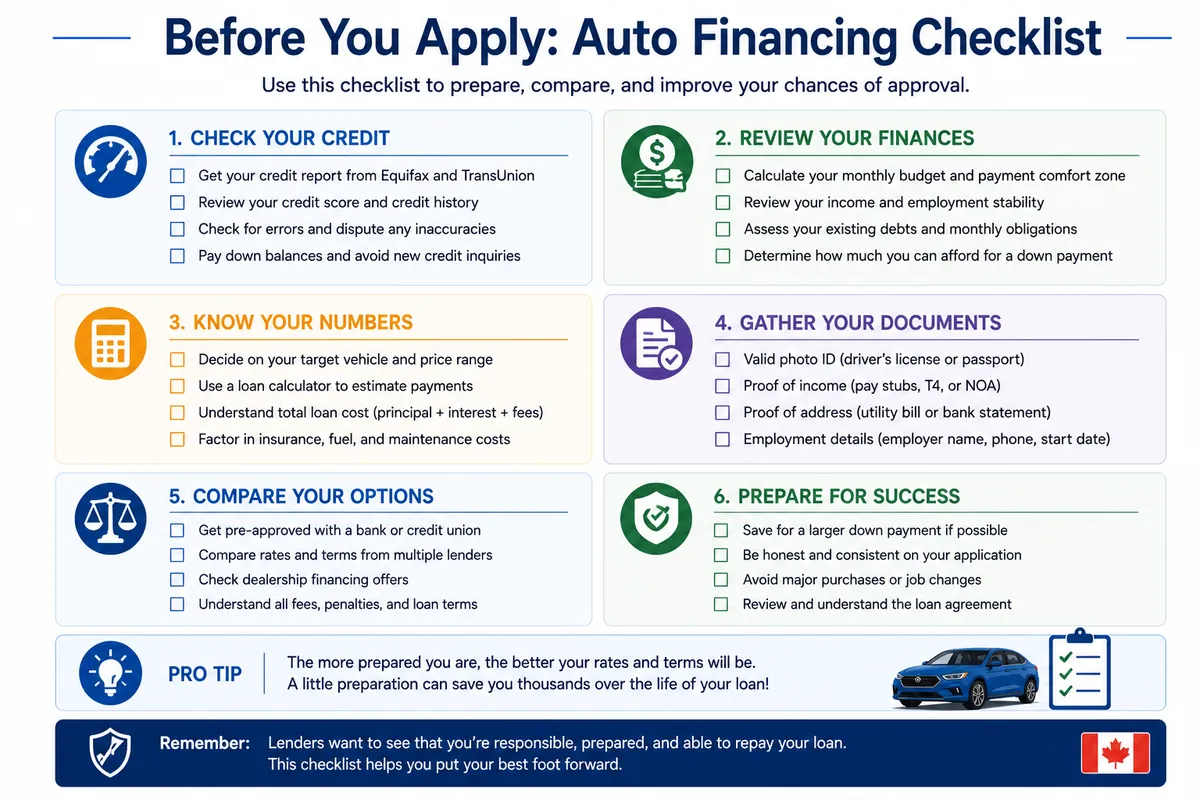

Common Mistakes to Avoid

| Mistake | Why It Matters |

|---|---|

| Focusing only on monthly payment | A low payment may come from a longer term, which can increase total cost |

| Choosing more vehicle than you can afford | Remember insurance, fuel, maintenance, registration, and emergency costs |

| Not reviewing the agreement | Always understand the amount financed, term, payment, interest, and total repayment |

| Applying without preparation | Have accurate personal, employment, income, and residence information ready |

| Ignoring your overall budget | A vehicle should support your life, not create unnecessary stress |

Common Mistake

Frequently Asked Questions

Your Next Steps

If you've read this guide, you now understand the major parts of the Canadian auto financing process. Before applying, review this checklist:

Budget

- Know what monthly payment fits your budget

- Consider insurance, fuel, maintenance, and ownership costs

Vehicle

- Research the type of vehicle you need

- Choose a realistic price range

Financing

- Understand interest, loan terms, and total borrowing cost

- Know which financing situation applies to you

Preparation

- Keep your information accurate

- Have documents ready if requested

- Ask questions before signing anything

When you're ready, AutoVoice Approval Match can help you explore financing opportunities based on your situation. Approval Match does not guarantee financing, but it can help you begin the process with clearer direction.